Random variates are random numbers that are generated according to a specific probability distribution. They are used in simulations to model real-world phenomena that follow certain statistical properties. For example, if you want to simulate the time between arrivals of customers at a store, you might use an exponential distribution to generate random variates that represent these inter-arrival times.

First our lib functions,

import math, random

import matplotlib.pyplot as pltInverse Transform¶

The inverse transform method is a technique for generating random variates from a given probability distribution. It relies on the cumulative distribution function (CDF) of the target distribution. The idea is to generate a uniform random number between 0 and 1, and then use the inverse of the CDF to transform this uniform random number into a random variate that follows the desired distribution.

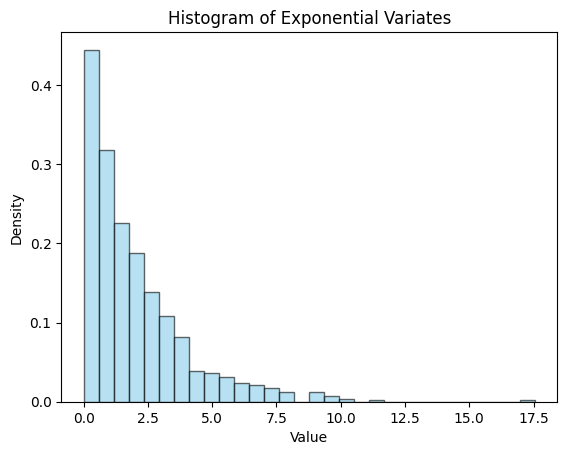

Exponential Distribution¶

def inverse_transform_exponential(uniform_numbers, rate_lambda):

exponential_variates = []

for u in uniform_numbers:

x = -math.log(1 - u) * rate_lambda # Inverse CDF for exponential distribution

exponential_variates.append(x)

return exponential_variatesuniform_numbers = [random.random() for _ in range(1000)]

exponential_variates = inverse_transform_exponential(uniform_numbers, rate_lambda=2)

print(exponential_variates[:10]) # Print the first 10 exponential variates[0.06877342512257881, 1.7777060238162274, 0.9622152298750513, 0.3100037728548614, 3.104922465310846, 0.6780781342546255, 0.22243631125437877, 3.997122118375026, 7.183874236446966, 0.36290596398493863]

plt.hist(

exponential_variates,

bins=30,

color="skyblue",

edgecolor="black",

density=True,

alpha=0.6,

)

plt.title("Histogram of Exponential Variates")

plt.xlabel("Value")

plt.ylabel("Density")